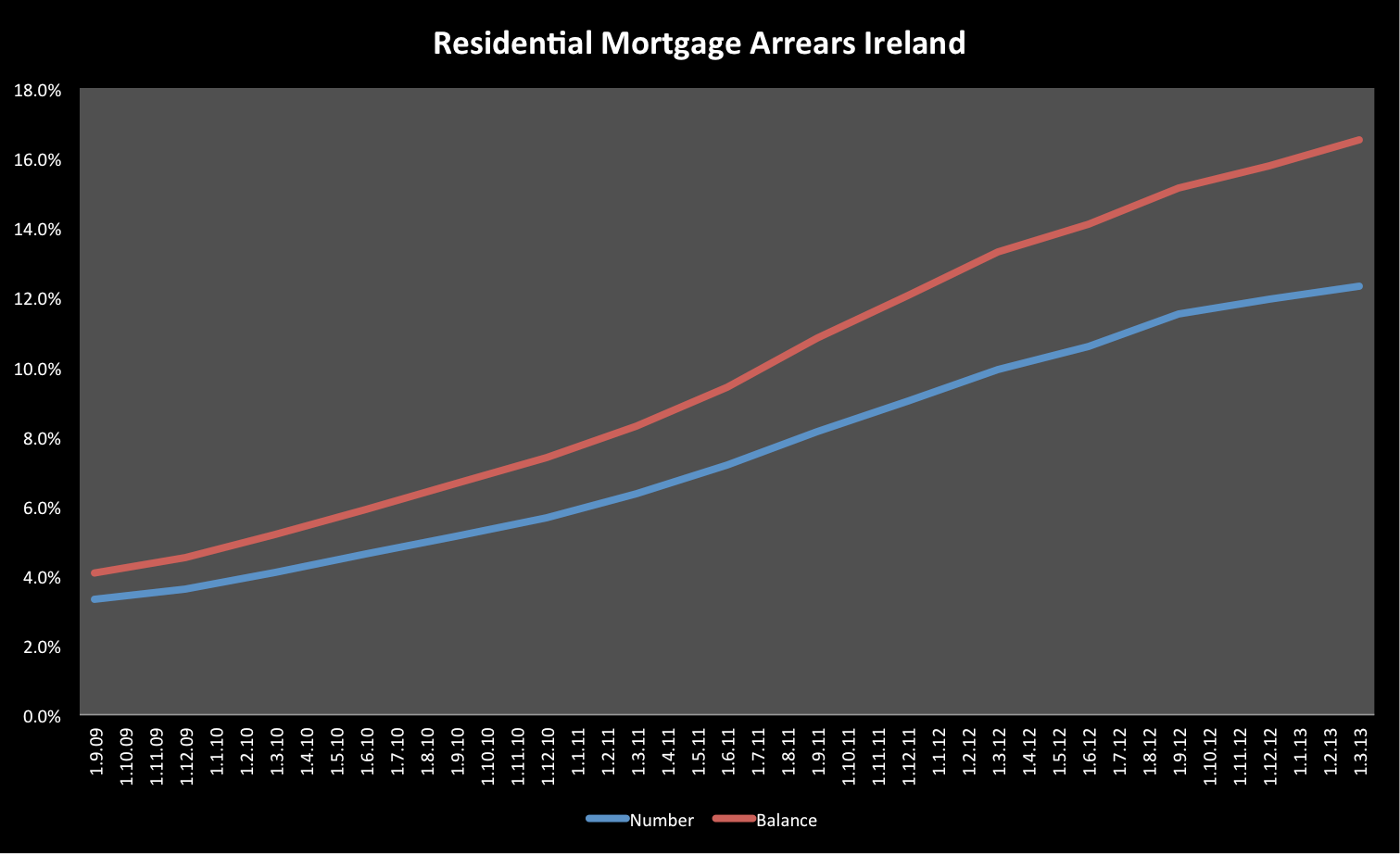

Irish residential and Buy to let mortgages are in a mess. The latest Central Bank data indicate that by value 16.5% of all residential mortgages are in arrears accounting for 12.3% of all mortgages. The charts below show the evolution of this situation. Note that these are only for residential mortgages. Buy to Let are a separate problem, and are commercial loans that if in default should be foreclosed on. There may well be an issue with cross collaterisation of these to residential but again thats a separate issue.

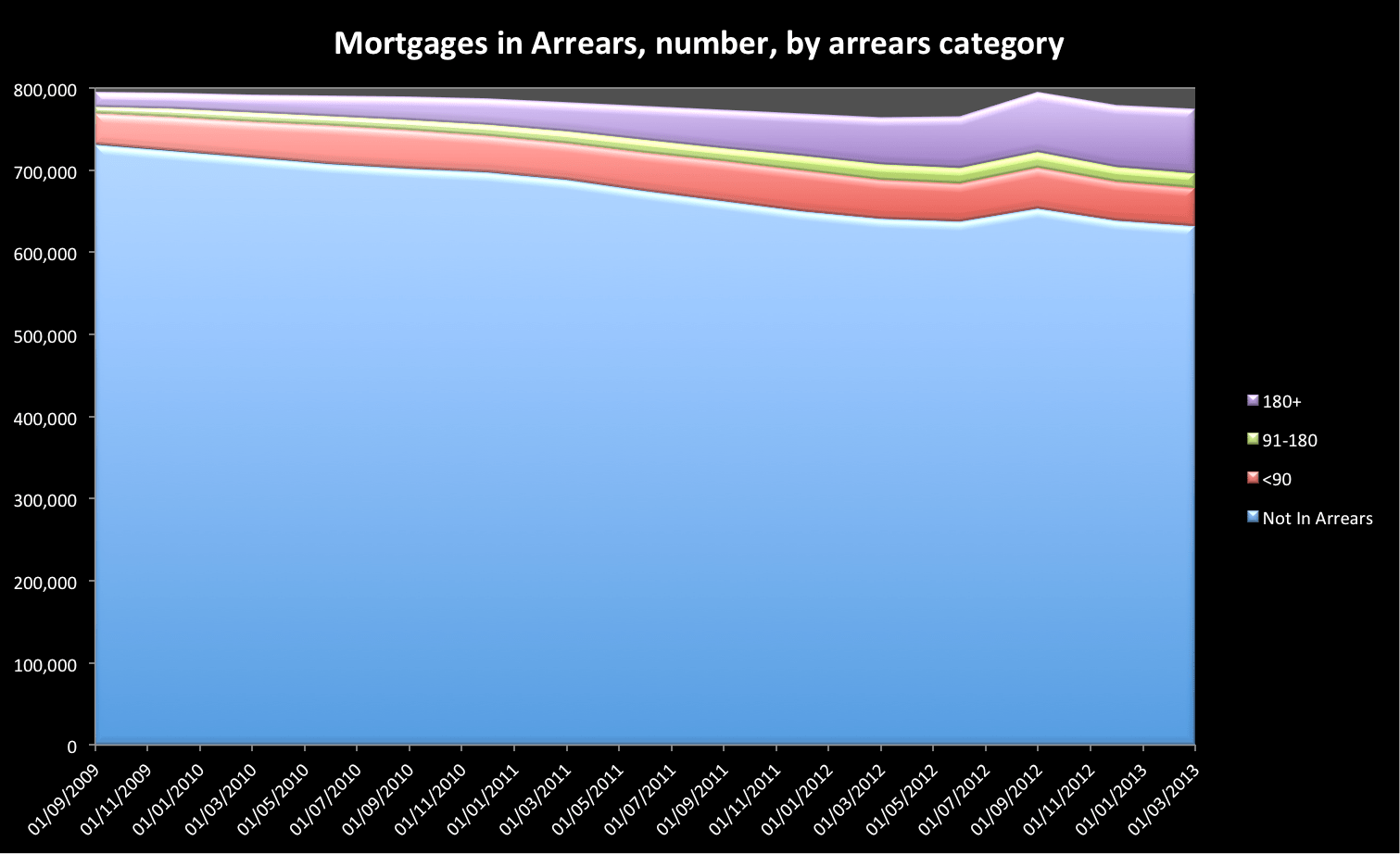

One of the issues that arises is “strategic default”, that is to say how many of these 142,000 mortgages in arrears are “wont pay” rather than “cant pay”. The simple answer is we do not know. That doesn’t stop the assumption that “its a lot”. Today we see in an otherwise excellent discussion by Davy stockbrokers on the banks the statement ” A growing culture of strategic non-payment of debt “. How do they know its growing? From what base? To what level?

The meme is that its 1/3 of arrears in default are “Strategic” , Wont Pay defaulters. This arises from a post by Professor Gregory Connor where he took US studies and tried to map the findings to Ireland. This is a difficult and thankless task but absent anything else its all we have.

In a parliamentary reply to a question on this issue the Minister for Finance stated his view (aka the Department of Finance view) on the 1/3 figure as ” The suggestion that the rising number of mortgage arrears is in part being driven by increased levels of strategic default, that is individuals deliberately withholding payments when they are in a position to service their debt in hope of gaining concessions from lenders, is wholly anecdotal and not based on any robust, structured, or in-depth analysis of the situation”

This then begs the question : where is this analysis? So far as I am aware there is none. A proper analysis of the issue of strategic or wont pay default would require the following, I contend.

- a survey of all defaulters, or a representative sample thereof.

- While this survey would have to originate from the issuing lenders it would have to be 100% clear and bulletproofed that no information whatsoever would return back from the analysis to the lender such that individual borrowers could be identified. Thus in all probability no official body should carry out the analysis or interpretation

- defaulters would need to be queried as to their present expenditure habits , with a view to ascertaining whether they were strategic and if so how and why

- to what extent are borrowers strategic in placing other loan repayments before mortgages or are they defaulting on many loans and using funds for ongoing living expenses

- to what extent are they not repaying due to pressure, either lack of same from the mortgage lenders or relatively greater from other

- the extent to which social and other pressures impact ; there is a good recent paper on this in SSRN

Now, it may be that this is already underway. But if its not then it should be. I am perfectly happy to undertake this research pro-bono, and I am sure that other academics would help. This information, the bare knowledge of who is defaulting and why, needs to be surfaced. We cannot devise strategies if we dont know the problem. We cant simply map the situation in the USA, with wildly different legal and economic systems, to Ireland.

Leave a Reply